{kind=link}

The Problem: Benefits Untapped and Costs Accumulating

Many hold the DiDi card yet observe little benefit from its promise; rewards lie dormant while fees and missed opportunities mount. This guide addresses those precise frictions and supplies a practicable route to greater yield. For readers seeking credit solutions alongside card optimisation, consider also reviewing didi prestamos as part of a broader financial plan.

Why Cardholders Fail to Maximize Benefits

Several causes impede advantage extraction: unclear program rules, infrequent use in qualifying categories, and insufficient attention to billing cycles and APR implications. A suboptimal credit score can reduce available offers through underwriting, and habitually treating the card as a mere payment token removes chance to accrue merchant-specific rebates or installment plan promotions. The remedy requires both policy knowledge and a modest alteration of transaction habits.

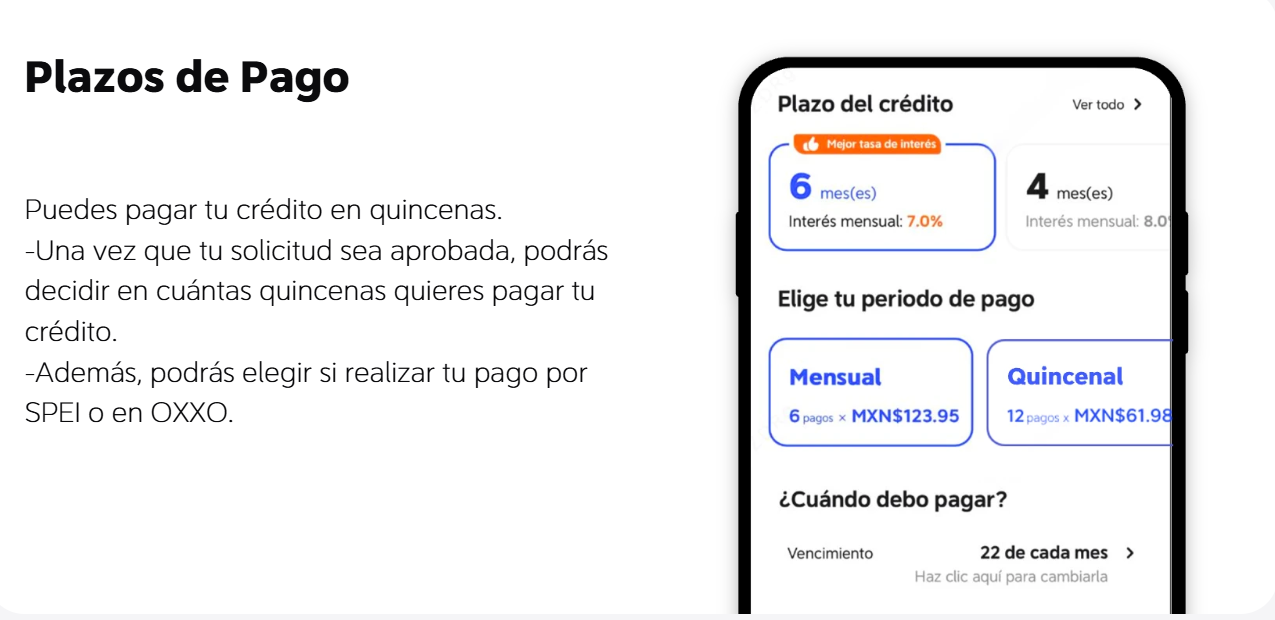

Concrete Steps to Increase Net Benefit

Begin with a concise audit of past three months’ statements. Note reward categories, payment dates, and any recurring fees. Thereafter adopt the following regimen:

– Align recurring bills (utilities, subscriptions) with the card’s billing cycle to concentrate spend where rewards multiply. – Prioritise purchases that yield elevated cashback or partner discounts; use a digital wallet that centralises offers and reduces friction. – Maintain on-time payments to preserve credit score and avoid APR penalties. Small, punctual payments lower long-run cost. – Use promotional installment plans selectively on larger purchases when the effective APR on cash is higher than a zero-interest installment offer. – Re-evaluate merchant offers quarterly; merchants and partners change frequently, and what was lucrative last quarter may be neutral now.

Common Mistakes and Sensible Alternatives

Cardholders often accept the default setup: no alerts, default categories, and passive oversight. This neglect generates missed rebates. Conversely, aggressive churn—opening and closing accounts to chase bonuses—invites underwriting scrutiny and can harm long-term credit prospects. For those needing liquidity beyond routine credit, compare standard card usage with tailored creditos en linea offers; certain short-term loans or lines of credit may prove less costly when viewed net of fees and reward capture.

Real-World Context and a Brief Anchor

In Mexico City, where ride-hailing and digital payments saw conspicuous expansion following the pandemic, many urban consumers adopted digital cards rapidly and, yet, seldom optimized them. This trend mirrors broader fintech uptake across Latin America and underscores the practical worth of small behavioural changes—aligning spend categories and calendar dates often yields results immediately noticeable on the monthly statement.

Risk Controls and Technical Notes

Keep a watchful stance on data privacy and transaction alerts. Reconcile statements weekly and contest unfamiliar charges without delay. Employ two-factor authentication for app access and be cautious when linking third-party aggregators that request full-line credentials. For larger purchases, evaluate the effective cost after rewards—account for instalment plan terms and any deferred interest that may be incurred.

Three Golden Metrics for Decision-Making

Use these evaluative criteria when judging strategies or tools: 1) Net Return Rate — measure cashback and discounts after fees to assess true yield. 2) Liquidity Impact — compare monthly cash flow demands with payment schedules and potential APR exposure. 3) Credit Health Effect — monitor credit score shifts that arise from utilization changes and new credit inquiries. These metrics orient choices toward clear, measurable outcomes rather than promising-sounding features.

Closing Reflection and Practical Resolution

Adoption of a disciplined routine—audit, align, and reassess—transforms the DiDi card from a passive instrument into an active yield generator. The lessons herein are modest yet effective; they require consistency rather than grand gestures. For those seeking a cohesive financial service that bundles card benefits with lending options, DiDi Finanzas appears naturally suited to bridge daily spending with available credit — a pragmatic solution for modern urban finance. —